Market Intelligence Brief: Support Breaks, Missiles Fly, and Markets Price a Longer War

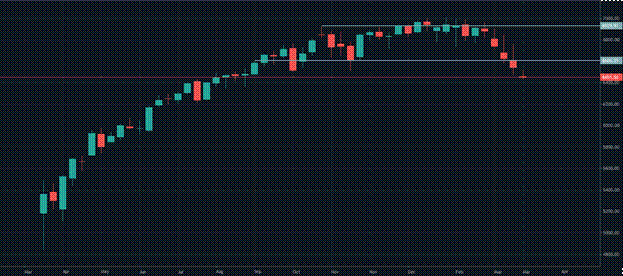

March 23, 2026 - The S&P 500 has broken clearly through its support level. The FTSE has breached its own. Germany 40 is down over 2%. Israel has signalled several more weeks of fighting. The support structures that held through four weeks of conflict have finally yielded.

The support levels that had been absorbing sustained geopolitical and inflationary pressure for four weeks have broken. The S&P 500 has now clearly broken through support that held, with varying degrees of stress, since October. The FTSE’s support level has been clearly breached. Germany 40 is down 2.22%. The FTSE is lower by 2.33%. Oil has risen on the ongoing missile standoff between the US and Iran, and the knock-on inflationary effects have sent markets sharply lower across the board. Israel has confirmed it intends to expand its attacks in Lebanon and has indicated there will be several more weeks of fighting against both Iran and Hezbollah. Monday opens the week not with cautious optimism or managed uncertainty, but with a confirmed and broad-based technical breakdown.

Support Breaks: What the Technical Shift Means

The S&P 500 holding its October-origin range through a month of conflict, Strait closures, infrastructure attacks, and central bank tightening signals was one of the more analytically significant features of March’s market action. The range held not because the news was good, but because buyers were repeatedly willing to step in at those levels, maintaining a floor beneath the market that had structural significance built over five months of trading.

That structural significance has now been removed. When a support level that has held through multiple waves of selling finally breaks, it does not merely represent a lower price. It signals that the buyers who had been defending the level have either exhausted their conviction, revised their fundamental assessment, or calculated that the risk of holding through further deterioration outweighs the case for recovery at that price. In the current context, all three motivations are plausible simultaneously.

The break is not a prediction of how far the market falls from here. Swift recoveries can follow support breaks if the catalyst that caused them reverses. They can also mark the beginning of a sustained decline if the conditions that caused the break persist or worsen. What the break does unambiguously is remove the structural reference point that had been defining the market’s lower boundary. Without that floor, the next meaningful area of demand must be located, and that process can take time and distance.

The FTSE’s simultaneous breach of its own support level is equally significant. The upward channel that had held throughout the conflict period, supported by the energy sector’s natural hedge and the index’s relative resilience, broke on Monday morning. Two major indices breaking through established technical levels simultaneously on the same catalyst reinforce the view that this is a broad-based repricing rather than a sector- or region-specific adjustment.

The Missile Standoff Continues and Extends the Timeline

The immediate catalyst for Monday’s move is the continuation and apparent intensification of the rhetorical standoff between the US and Iran over missile capabilities and willingness to use them. The characterisation of the situation as a “we’ll fire more missiles than you” exchange captures its essence: a confrontation that is no longer building toward resolution but actively maintaining and reinforcing the conditions of conflict.

A missile standoff of this rhetorical intensity serves the interests of both parties in specific ways. For the US administration, maintaining a posture of overwhelming force potential provides domestic political cover for the conflict’s lack of swift conclusion. For Iran, the standoff narrative allows the regime to present itself as holding its ground against a substantially more powerful adversary, which serves internal political purposes even as the country absorbs military pressure.

For markets, the standoff’s continuation does specific damage. It directly undermines the de-escalation narrative that Netanyahu constructed on Friday. Energy markets that had eased on the prospect of reduced infrastructure attacks are now processing the signal that the confrontation is not de-escalating at all; it is sustaining at an elevated level of threat intensity. Oil going higher on Monday is the commodity market’s straightforward read of that reset.

Israel’s Timeline Signal: Several More Weeks of Fighting

Israel’s statement that there will be several more weeks of fighting against Iran and Hezbollah is the most direct timeline signal the conflict has produced. Previous assessments of duration had come from the US side and were framed in optimistic terms that the subsequent events repeatedly failed to validate. A statement from Israel about the expected duration of its own operations is a different category of information: it is the party conducting the operations providing its own planning horizon.

Several more weeks carry specific implications for how markets must recalibrate their expectations. The scenario in which the conflict concluded within days or a fortnight, which had been implicitly embedded in the market’s cautious holding pattern across much of the past three weeks, is no longer credible. A conflict with several more weeks of expected fighting from one of its primary protagonists is one the market must price over a substantially longer horizon than the range-holding behaviour of recent sessions implied.

The Lebanon expansion adds a further dimension. Hezbollah’s involvement draws the conflict further into Lebanese territory and extends the geographic scope of the military operation. Each extension of geographic scope adds complexity to any potential diplomatic resolution and introduces additional parties whose interests must be addressed in any settlement. The diplomatic horizon, already distant, recedes further as the theatre of operations expands.

The cumulative message from Monday’s developments is that the market had been pricing insufficient duration and insufficient scope. The support level breaks reflect that recalibration. Pricing a conflict that lasts several more weeks, with an expanding geographic scope and a sustained rhetorical standoff, requires lower equity valuations and higher oil and safe-haven asset pricing than the range that had held through the previous three weeks.

European Equities: The Sharpest Losses of the Conflict Period

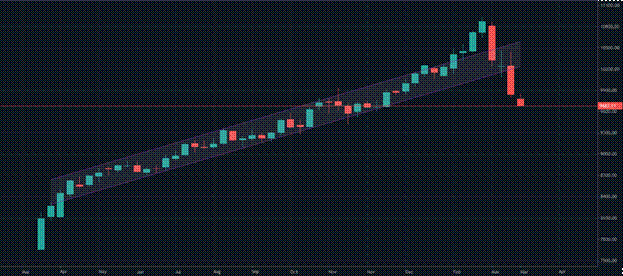

Germany 40 is down 2.22%, and the UK 100 is lower by 2.33%, the sharpest simultaneous decline the two indices have registered during the conflict. The FTSE’s 2.33% fall is particularly notable given the energy sector’s natural hedge that had cushioned the index through previous waves of selling. When even the FTSE takes the most severe losses of the conflict period, it signals that the breadth of Monday’s selling has overwhelmed the sector-specific support mechanisms that provided partial protection in earlier sessions.

The DAX’s 2.22% decline continues its pattern of absorbing European selling pressure acutely, driven by Germany’s industrial energy intensity, LNG supply exposure, and trade dependence on a global economy that is operating under sustained disruption. The index has now given back a substantial portion of the recovery it achieved from the conflict’s initial lows, and the break below support removes the technical framework that had been providing structure to the European equity decline.

The FTSE’s breach is the more significant in the context of the conflict’s history. The index had demonstrated remarkable structural resilience over four weeks of pressure, consistently finding support at the lower boundary of its upward channel. The channel has now been broken, removing one of the more reliable features of the European equity landscape since February.

EURUSD and Currency Markets: Dollar Pressure Intensifying

EURUSD is down 0.72%, and GBPUSD is lower by 0.56%, both reflecting intensifying dollar safe-haven demand as the conflict’s extension and escalation feed the flows that have been supporting the dollar throughout the month. The moves are the largest single-session declines for both pairs in recent sessions and suggest that currency participants are repricing the conflict’s duration in the same way that equity markets are.

USDJPY is up 0.23%, continuing the dollar-supportive pattern while the Bank of Japan’s tightening bias provides a mild counterweight. The dollar’s safe-haven advantage is asserting itself decisively amid a shift in the risk environment.

The euro faces specific pressure from the combination of the conflict’s extension and the European inflation and rate-hike implications it compounds. A longer conflict means sustained energy cost pressure, which means a more sustained case for ECB tightening, which creates its own growth headwind for the eurozone. The currency market is processing that chain with the 0.72% move.

The Market Has Changed Character

The most important analytical observation of Monday morning is not any single number but the character of the move. For four weeks, the market had been operating in a mode of managed uncertainty: absorbing each new development within established technical structures, finding support at defined levels, and maintaining a framework that implied the conflict’s impact was containable within a range. Monday’s session changes that character.

When support levels break simultaneously across US and European indices, when the breaks are confirmed rather than tested and recovered, and when the catalyst is a combination of extended conflict timeline and intensifying rhetorical standoff rather than a single identifiable shock, the market is communicating something structural rather than tactical. The range-holding phase of the conflict’s market impact appears to be over. The repricing phase, in which the market establishes new, lower reference points appropriate to a longer and broader conflict, seems to have begun.

That transition does not eliminate the possibility of recovery. If the several more weeks of expected fighting conclude more swiftly than the statement implies, or if a diplomatic channel opens unexpectedly, the market can recover from technical break levels quickly. What it does is remove the prior support structure as the basis for that recovery and require the establishment of a new framework.

The Bottom Line

Monday opens with the clearest structural market development of the conflict period: confirmed support breaks across the S&P 500, FTSE, and DAX simultaneously, driven by the continuation of the US-Iran missile standoff, Israel’s signal of several more weeks of fighting, and the inflationary consequences of higher oil filtering into a market that had been holding its ground.

The support structure that absorbed four weeks of geopolitical pressure has yielded. The conflict’s expected duration has been extended explicitly by one of its principal parties. Oil is higher. EURUSD and GBPUSD are under their sharpest single-session pressure of recent weeks. No major earnings are scheduled to provide any counter narrative.

The market is not experiencing a single event shock of the kind that produced Monday’s extraordinary reversal earlier in the month. It is experiencing the accumulated weight of a conflict that has lasted longer, escalated further, and caused more economic damage than the range-holding behaviour of the past three weeks had implicitly priced in. The support breaks are the honest market expression of that reassessment. Where the new equilibrium lies will depend on how the next several weeks of fighting unfold and whether any diplomatic mechanism emerges to provide an alternative trajectory.

Lunaro Financial Services Limited (trading as ‘Lunaro’) is an execution-only service provider. This material is a marketing communication and is provided for general information and educational purposes only. It does not take into account your personal circumstances, objectives or needs. Any opinions are those of the author at the time of writing and may change without notice. Nothing in this material constitutes (or should be construed as) financial, investment, legal, regulatory or tax advice, or a recommendation to engage in any investment activity. You should not rely on this material when making investment or trading decisions.

This material has not been prepared in accordance with legal requirements designed to promote the independence of investment research and is not subject to any prohibition on dealing ahead of the dissemination of investment research. Lunaro may deal as principal and/or have an interest in the financial instruments or markets referred to in this material in the ordinary course of its business, including at or around the time of publication, and does not seek to take advantage of this material prior to its dissemination.

While reasonable care has been taken in preparing this material, no representation or warranty is made as to its accuracy or completeness and Lunaro accepts no liability for any loss arising from any use of, or reliance on, this material.

Approximately 80% of retail investor accounts lose money when trading CFDs with this provider. You should consider whether you can afford to take the high risk of losing your money.

Comments

Post a Comment