Market Intelligence Brief: Kharg Island, Ground Troops, a Deal “Fairly Quickly,” and Inflation Expectations That Shocked

March 30, 2026 - Reports of Trump considering seizing Iran’s Kharg Island, officials describing ground troop preparations, and a presidential promise of a deal “fairly quickly” opened the week with maximum ambiguity. Markets are modestly higher. The Nasdaq has bounced off its 23,000 support level. And eurozone inflation expectations just printed nearly double the forecast.

The week opens with a set of developments that would be significant individually and, collectively, constitute the most contradictory single morning of the conflict period. Trump is reportedly considering seizing Kharg Island, Iran’s primary oil export terminal, which would represent a dramatic military escalation. Officials have described troops preparing for ground operations, another major escalation step. And Trump himself has said a deal could be reached “fairly quickly,” his most optimistic framing since “ahead of schedule” in the conflict’s second week. Market reactions to Sunday night’s news were muted, and futures are modestly higher this morning. The characterisation that Trump’s comments carry too much “maybe” to allow investors to form a clear view is precise: the ambiguity in the messaging is now so embedded in the conflict’s communication pattern that participants are applying consistent scepticism regardless of whether the signal is bullish or bearish.

Against that backdrop, the eurozone Consumer Price Expectations reading for March has arrived at 43.4 against a forecast of 24.5 and a previous reading of 26.2. The figure, nearly double the forecast and materially above the prior reading, is the single most significant piece of scheduled economic data released during the conflict period. It tells us directly how European households expect prices to move in the months ahead, and the answer is that they expect them to move sharply higher.

Kharg Island and Ground Operations: The Escalation Reports

Kharg Island is not a marginal target. It is the terminal through which approximately 90% of Iran’s oil exports pass. Seizing or turning it off would represent a qualitative escalation from air and missile operations into physical territorial control of critical economic infrastructure. The military, logistical, and diplomatic complexity of such an operation, in terms of the forces required, the risks involved, and the responses it would likely generate from Iran and regional actors, is substantially greater than anything the conflict has involved to date.

Officials describing troops as preparing for ground operations adds operational credibility to what might otherwise be treated as speculative reporting. Ground operations represent the most significant potential escalation of the conflict since its beginning, involving risks that air and missile strikes do not: territorial presence, potential for direct engagement with ground forces, higher casualty exposure, and the political difficulty of withdrawal once committed. A conflict that has been conducted primarily through air power and missiles for five weeks would enter a materially different phase if ground troops were deployed.

Markets received these reports with muted reaction on Sunday night, and futures are only modestly higher this morning rather than sharply lower. Two interpretations of the muted reaction are available. The first is that the market has applied such consistent scepticism to US communications about the conflict that even reports of potential ground operations are being treated as preparation for negotiating leverage rather than genuine operational intent. The second is that “fairly quickly” on a deal counterbalances the ground operation reports in the market’s immediate assessment, leaving the net signal ambiguous rather than clearly negative.

“Fairly Quickly” and the Maybe Problem

Trump’s statement that a deal could be reached “fairly quickly” is his most optimistic framing of the conflict’s diplomatic trajectory in several weeks. It arrives alongside reports of ground troop preparations and considerations of seizing Kharg Island, producing the specific combination that investors find most difficult to interpret. Is the deal statement the real signal, and does the military report the leverage being applied to achieve it? Or are the military reports the real development, and the deal statement the messaging designed to prevent a sharper market reaction?

The “too much maybe” characterisation is the market’s honest response to that ambiguity. A message that can mean either “we are close to a deal” or “we are preparing a major military escalation to force a deal”, depending on which part of the communication is treated as primary, is a message with very wide confidence intervals. Wide confidence intervals in a market already positioned for uncertainty produce muted reactions rather than directional moves. The modest morning futures gains reflect the balance of the two signals rather than a clear verdict on either.

The “fairly quickly” framing also fits within a credibility pattern the market has been calibrating throughout the conflict period. “Ahead of schedule” on March 9th, “wants a deal so badly” in late March, “fairly quickly” today. Each optimistic framing has been followed by developments that contradicted it. The market’s muted response reflects not dismissal but discount: the probability assigned to “fairly quickly” being accurate is lower than it would have been if this were the first such statement rather than the latest in a series.

Eurozone Inflation Expectations at 43.4: The Most Important Economic Data of the Conflict Period

The eurozone Consumer Price Expectations reading for March, published this morning at 43.4 against a forecast of 24.5 and a previous reading of 26.2, is the single most significant scheduled economic data point to emerge from the conflict. The magnitude of the beat, nearly double the forecast, and the magnitude of the increase from the previous reading, from 26.2 to 43.4, together paint a picture of European consumer inflation expectations that has moved sharply and rapidly in response to the conflict’s energy cost impact.

Consumer Price Expectations surveys measure not current inflation but forward-looking inflation sentiment: how much higher households expect prices to be in the coming months. An index reading of 43.4 indicates a substantial majority of respondents expecting prices to rise significantly. The distance between the forecast of 24.5 and the actual of 43.4 suggests that even those economists projecting above-baseline inflation expectations were not anticipating the scale of the shift in European household sentiment that the conflict’s energy costs have produced.

The ECB’s policy framework places significant weight on inflation expectations as a leading indicator of future price behaviour. When expectations become unanchored to the upside, the risk is that they become self-fulfilling: workers demand higher wages to compensate for expected higher prices, businesses raise prices in anticipation of higher costs, and the expectation-driven inflation compounds the supply-side inflation that initiated it. An expectation reading this far above forecast is the kind of data that makes the ECB’s tightening bias, flagged three weeks ago alongside those of the Bank of England and the Bank of Japan, materially more urgent.

For equity markets, the implications are direct. A Consumer Price Expectations reading that nearly doubles the forecast and the previous level simultaneously increases the probability of near-term ECB rate action. It reduces the real purchasing power of European consumers in forward assessments. Both of those channels are equity-negative. The DAX’s marginal decline of 0.13% this morning, whilst the broader European and US tone is modestly positive, may partially reflect this specific data point landing on top of the conflict’s existing German vulnerabilities.

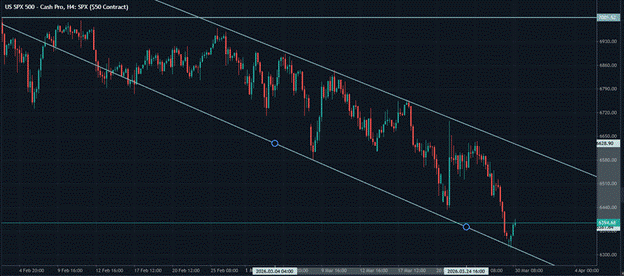

The Nasdaq Bounces From 23,000

The Nasdaq 100 has reached the 23,000 support level identified in last Thursday’s commentary and bounced higher, currently trading around 23,224. The identification of 23,000 as the next major support, derived from the August-September period of last year when the market bounced from those levels multiple times, has proven analytically relevant in the first test.

Whether the bounce develops into a sustained recovery or constitutes a reprieve depends on the diplomatic variable that the chart cannot price. The lower lows and lower highs pattern that has defined the S&P 500’s trajectory through the conflict period remains intact; the bounce from 23,000 does not yet constitute a higher low. For the bounce to signal a genuine change in trend character, the Nasdaq would need to extend recovery to a level above its previous rally peak before the next decline. That has not yet occurred.

The conditional observation in this morning’s analysis is precise: whether 23,000 becomes a prominent support level depends on how fast the US can reach a deal with Iran. Should the war continue at its current pace, the level could be broken. That conditional framing captures the analytical reality: the technical support is grounded in historical precedent, but its relevance in the current environment is secondary to the geopolitical variable that will determine whether buyers at 23,000 find their conviction sustained or overwhelmed by further conflict-related deterioration.

The S&P 500 similarly shows a lower highs and lower lows pattern with a bounce from its recent lower bound. Both indices have retraced somewhat from their recent lows, but characterising that retracement as potentially temporary rather than structurally significant is appropriate given the absence of any confirmed diplomatic progress to underpin it.

European Equities: The DAX Finding Support at 22,000

The DAX has found support at the 22,000 level, failing to make a new low, which represents a modest constructive development from Thursday’s sharp decline. The EU markets are described as more resilient than US futures in the current session despite being dragged lower by SPX and NDX weakness over the preceding sessions. The DAX’s fractional decline of 0.13% and the FTSE’s 0.64% gain reflect a European market that is holding rather than continuing to fall.

The 22,000 level’s significance as support should be treated with the same conditional framing applied to the Nasdaq’s 23,000. Historical support levels provide reference points but not guarantees, particularly in an environment where the primary driver of asset prices is a geopolitical situation that has been overriding technical structures with regularity throughout the conflict period.

The FTSE’s 0.64% gain is the more notable European move and reflects both the modestly positive tone from US futures and the partial restoration of the energy sector’s contribution, as oil remains elevated. The index remains below the support level it breached last week, and the gain should be read as a partial recovery within a broken structure rather than a return to the constructive trajectory that preceded the break.

Powell Speaks: The Session’s Critical Scheduled Event

Fed Chair Powell’s speech is scheduled for 15:30, and arrives in a context that makes it the most consequential central bank communication since the conflict began. The eurozone Consumer Price Expectations reading published this morning provides immediate and stark context for what the Fed Chair may say about the US inflation outlook and policy path.

Powell has not spoken substantively about the conflict’s economic implications since the situation escalated. The market’s tightening bias assessment has been inferred from the ECB, Bank of England, and Bank of Japan’s simultaneous hold-with-hawkish-guidance decisions. A direct statement from the Fed Chair about the conflict’s inflation impact and the Fed’s policy reaction function would be the clearest central bank input of the entire conflict period. How he chooses to frame the position, and whether he provides any guidance on the timeline for potential action, will be the session’s primary market-moving event.

The Bottom Line

Monday opens the sixth week of the conflict with the most ambiguous combination of signals yet: potential ground operations and Kharg Island seizure reports alongside “fairly quickly” on a deal, a eurozone inflation expectations reading nearly double its forecast, the Nasdaq bouncing from its 23,000 support level, and Powell speaking in the afternoon with the conflict’s inflation implications as the unavoidable backdrop.

Futures are modestly higher in a reflection of the balance of the week’s opening signals rather than a directional verdict on any of them. The muted character of the reaction to Kharg Island reports and ground troop preparations tells the story of five weeks of conditioning: the market has learned to treat even significant escalation signals as provisional until confirmed and to balance them against the optimistic statements that typically accompany them.

The eurozone CPI Expectations reading is the session’s most unambiguous input. At 43.4, against a forecast of 24.5, it tells the ECB and equity markets in plain terms what European households expect from prices in the months ahead. That reading cannot be attributed to “maybe.”

Lunaro Financial Services Limited (trading as ‘Lunaro’) is an execution-only service provider. This material is a marketing communication and is provided for general information and educational purposes only. It does not take into account your personal circumstances, objectives or needs. Any opinions are those of the author at the time of writing and may change without notice. Nothing in this material constitutes (or should be construed as) financial, investment, legal, regulatory or tax advice, or a recommendation to engage in any investment activity. You should not rely on this material when making investment or trading decisions.

This material has not been prepared in accordance with legal requirements designed to promote the independence of investment research and is not subject to any prohibition on dealing ahead of the dissemination of investment research. Lunaro may deal as principal and/or have an interest in the financial instruments or markets referred to in this material in the ordinary course of its business, including at or around the time of publication, and does not seek to take advantage of this material prior to its dissemination.

While reasonable care has been taken in preparing this material, no representation or warranty is made as to its accuracy or completeness and Lunaro accepts no liability for any loss arising from any use of, or reliance on, this material.

Approximately 80% of retail investor accounts lose money when trading CFDs with this provider. You should consider whether you can afford to take the high risk of losing your money

Comments

Post a Comment